Caixabank (Go to Home)

Caixabank (Go to Home)

Print page

Print page

26 July 2019

|

min read

CORPORATE

National

VALENCIA

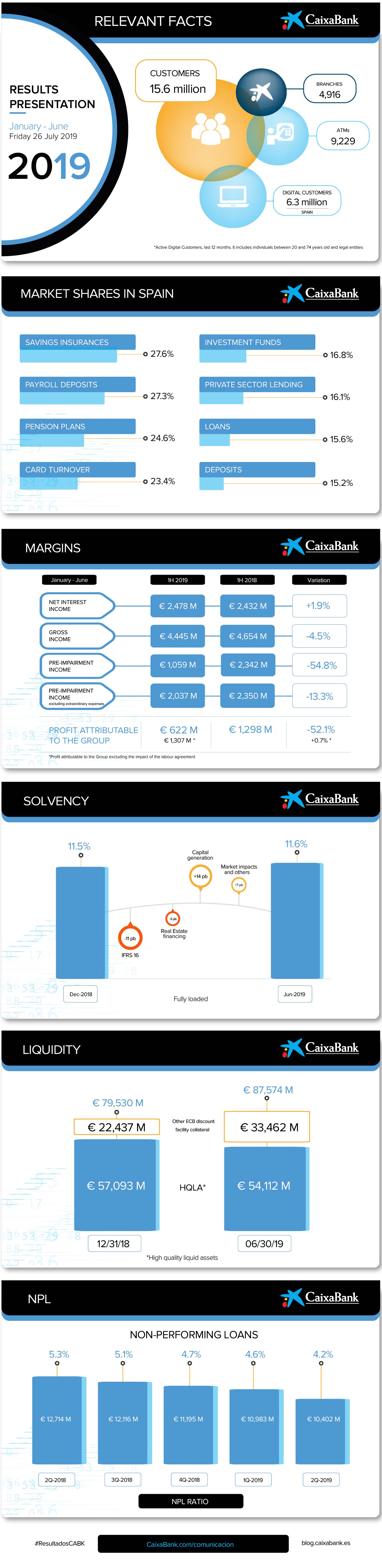

CaixaBank posts half-year profit of €622 million after absorbing the cost of the labour agreement

Gonzalo Gortázar, CEO of CaixaBank

Gonzalo Gortázar, CEO of CaixaBank

- The Group’s earnings are largely a product of the labour agreement reached in the second quarter, which will pave the way for 2,023 voluntary redundancies at a cost of €978 million (€685 million, net).

- Excluding this impact, earnings for the first six months of the year would be €1.31 billion (+0.7%). Earnings from the banking and insurance business amount to €295 mil-lion (+21.4% excluding the impact of the labour agreement).

- The Bank surpasses €600 billion (+4.9%) in total loans and deposits for the first time, on the back of strong commercial performance: customer funds increase to €380.86 billion (+6.2% in 2019), gross loans and advances to customers grow to €230.87 billion (+2.7% in the year) and the performing portfolio gains 3.3%.

- The non-performing loan ratio falls to 4.2% (-46 basis points in the first half of the year). Meanwhile, non-performing loans are down €793 million in the first six months (down €581 million in the quarter) to €10.4 billion, in response to active portfolio man-agement policies.

- CaixaBank accelerates the transformation initiatives laid out in its Strategic Plan, bringing forward to June 2020 the objective of having 600 ‘Store’ branches. Following the signing of the labour agreement, the entity confirms its commitment to financial inclusion in rural areas with the consolidation of its network of 1,081 rural offices.

- Total liquid assets amount to €87.57 billion, up €8.04 billion in the year thanks to the positive performance of the commercial funding gap and the fact that new issuances have outpaced maturities.

- The Bank reports a Common Equity Tier 1 (CET1) ratio of 11.6% at 30 June. Excluding the negative impact of -11 basis points due to the first-time application of IFRS 16 and the impact of -5 basis points due to the reduction in credit risk requirements for financing real estate assets, the ratio gained 14 basis points in the first six months from organic capital generation and a further 7 basis points from the positive performance of the market and other impacts.

- CaixaBank cements its leadership in digital banking, with 6.3 million digital customers in Spain (59.4% of total customers). Meanwhile, CaixaBank has been named Best Bank in Spain 2019, Best Bank for Corporate Responsibility in Western Europe 2019 and Best Bank Transformation in Western Europe 2019 by British publication Euromoney.

- CaixaBank completes the sale of its stake in Repsol in the second quarter.

The CaixaBank Group, with Jordi Gual as Chairman and Gonzalo Gortázar as CEO, reported a net attributable profit of €622 million in the first half of 2019, down 52.1% on the same period of 2018. Shaping this performance was the labour agreement reached in the second quarter, which generated an expense of €978 million (€685 million, net). Excluding this impact, profit would be up 0.7% on the same period of 2018 to reach €1.31 billion, while ROTE would have been 9.4%.

Net interest income for the first half of the year came to €2.48 billion (+1.9% on the same period of 2018). The performance here was largely down to the increase in income from lending activity, aided by a reduction in retail and institutional financing costs. The Group’s core revenues remained stable year on year but were up quarter on quarter (+1.5%), thanks mainly to the increase in commissions and income under insurance contracts.

Fee and commission income came to €1.25 billion, down 3.5% on the same period of 2018. In this regard, banking services, securities and other fees amounted to €719 million (-3.0%), impacted by a reduction in one-off investment banking transactions, among other factors.

Dividend income from the investee portfolio included a Telefónica dividend of €104 million in the second quarter of both years. The second quarter of 2019 also featured €46 million (gross) in dividends from BFA.

Share of profit of companies accounted for using the equity method was down €294 million (-58.4%) year on year, principally due to the fact that CaixaBank no longer reports earnings from BFA and Repsol (€312 million in 2018) in 2019. Excluding this impact, the performance would have been positive (+9.4%). CaixaBank also completed the sale of its stake in Repsol in the second quarter.

Trading income came to €261 million (-10.9%) and included the realisation of capital gains from fixed income assets in the second quarter, among other impacts. In 2018 it also included the repricing of BPI’s stake in Viacer as part of its divestment process and the result of the hedging transactions in connection with the subordinated bonds redeemed ahead of maturity.

The second quarter also included the contribution to the Single Resolution Fund of €103 million (€97 million in 2018).

Sustained growth in lending and customer funds over the first half of the year

The CaixaBank Group managed to surpass €600 billion in total loans and deposits for the first time (customer funds + gross lending activity), up 4.9% thanks to healthy levels of commercial activity. Customer funds increased to €380.86 billion (+6.2% in 2019). Within this category, on balance-sheet funds amounted to €276.88 billion (+6.7%).

Demand deposits totalled €189.95 billion. The growth here (+9.0% in the year and +5.5% in the quarter) was partly a result of the seasonal impact of double salary payments and the strength of the Bank, which now has over 4 million direct payroll deposits.

Highlights for the period include an increase in liabilities under insurance contracts (+4% in the year and +0.9% and in the quarter), thanks to healthy product portfolio performance and the Bank’s ability to adapt to customer needs. Unit Linked products also fared well, growing 16.6% in the year.

Assets under management rose to €98.2 billion. The annual performance (+4.5%) was largely down to good market performance following the slump seen at the end of the fourth quarter of 2018. Assets under management in mutual funds, portfolios and SICAVs amounted to €66.51 billion (+3.1% in the year, stable in the quarter), while assets under pension plans totalled €31.69 billion (+7.7% in the year and +2.3% in the quarter). In Spain, CaixaBank holds a market share of 16.8% and 24.6% for mutual funds and pension plans, respectively.

Meanwhile, gross loans and advances to customers stood at €230.87 billion (+2.7%), while the performing portfolio has gained 3.3% in the year to date. Excluding the seasonal impact of pension prepayments made in June (€1.68 billion), the performing portfolio would be up 2.5% in the year to date.

Loans to individuals excluding residential mortgages were up 5.8% in 2019 and in the quarter, on the back of strong consumer lending activity (+8.2% in the year and +4.7% in the quarter) and the positive seasonal impact of pension prepayments in the second quarter. Financing of corporates and SMEs (excluding real estate developers) is up 4.3% in 2019 (+2.5% in the quarter).

Non-performing loans fall to 4.2%

The NPL ratio was down to 4.2% (-46 basis points in the first six months), while NPLs shed €793 million in the first half of the year (-€581 million in the quarter) to reach €10.4 billion. The NPL coverage ratio is 54%.

The portfolio of net foreclosed real estate assets available for sale in Spain amounted to €863 million (+€123 million in the year and +€50 million in the quarter).

The portfolio of Spanish rental real estate assets stood at €2.33 billion (-€150 million in the year and -€79 million in the quarter), while total sales of real estate assets in 2019 came to €232 million.

Insolvency allowances totalled €204 million, down 17.6% on the same period a year earlier.

Excellent liquidity position and solvency

Total liquid assets amounted to €87.57 billion at 30 June, up €8.04 billion in the year due to the positive performance of the commercial funding gap and the fact that new issuances have outpaced maturities.

Meanwhile, the Group’s average Liquidity Coverage Ratio (LCR) at 30 June 2019 was 195%, well above the minimum requirement of 100% applicable as of 1 January 2018.

The balance drawn under the ECB facility, which had reached €28.18 billion at 31 March 2019, was down to €14.77 billion at 30 June (-€13.41 billion in the year due to the partial early repayment of the TLTRO II).

The Common Equity Tier 1 (CET1) ratio was 11.6% at 30 June. Excluding the impact of -11 basis points due to the first-time application of IFRS 16 and the impact of -5 basis points following the reduction in credit risk requirements for financing real estate assets, the ratio gained 14 basis points in the first six months from organic capital generation and a further 7 basis points from the positive performance of the market and other impacts. The performance of the capital ratio is in line with the objective envisioned in the 2019-2021 Strategic Plan.

CaixaBank, a benchmark in digitalisation

CaixaBank has consolidated its leadership of the digital banking market with 6.3 million digital customers in Spain (59.4% of total customers).

In addition, CaixaBank has accelerated its transformation initiatives laid out in its Strategic Plan, bringing forward to June 2020 (originally December 2021) its Strategic Plan objective of having 600 ‘Store’ branches. The Bank has also confirmed its commitment to financial inclusion in rural areas with the consolidation of its network of rural offices. Today, the Bank has 1,081 AgroBank branches in Spain, located in towns with less than 10,000 inhabitants. More than 2,000 towns and villages in Spain have a CaixaBank Group branch.

CaixaBank has recently been named Best Bank in Spain 2019, Best Bank for Corporate Responsibility in Western Europe 2019 and Best Bank Transformation in Western Europe 2019 by British publication Euromoney. The three awards are a testament to the Bank’s ongoing transformation in recent years to become the leading entity in retail banking and digital banking in Spain and Portugal, and a benchmark for socially responsible banking in Europe.

{kind=link}