Print page

Print page

July 27th, 2018

CORPORATE |

National

| VALENCIA

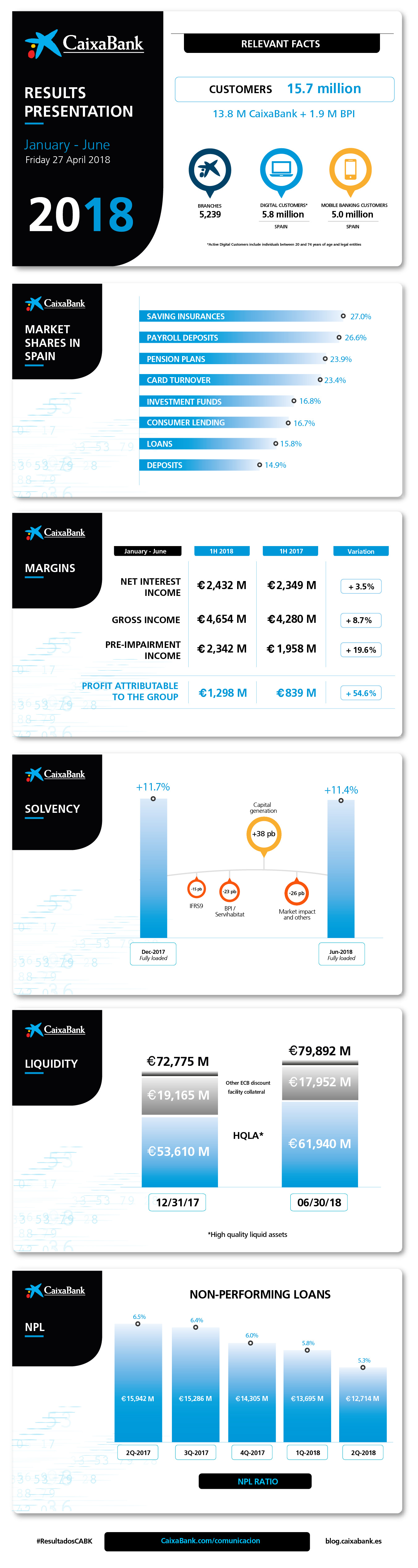

CaixaBank reports net of €1,298 million while growing customer funds by 4.8%

{kind=link}

{kind=link}

Gonzalo Gortázar, CEO at CaixaBank

Gonzalo Gortázar, CEO at CaixaBank

- The Group’s results are based on increased revenues, with gross income up 8.7% to €4,654 million, driven by strong performance of the core banking business (€4,091 million, up 4.5%).

- Profitability at the CaixaBank Group (ROTE) climbs to 10.4%, within the 9-11% target band envisioned in the Strategic Plan for 2018, while recurring ROTE from the banking and insurance business segment is 12%, yielding a result of €1,121 million.

- Non-performing loans are down €1,591 million in the year (down €981 million in the quarter), with the NPL ratio falling to 5.3% (6.5% in June 2017). The coverage ratio rises to 56%.

- Customer funds amount to €366,163 million (up 4.8% in 2018, or €16,705 million), and loans and advances to customers stand at €225,744 million (+0.8% in the year). The performing portfolio grows6% (€+3,366 million).

- Net interest income was up 3.5% to €2,432 million; fee and commission income totalled €1,293 million (+3.3%); and income and expense under insurance and reinsurance contracts climbed 21% to €282 million.

- Income from equity investments totalled €415 million. This includes earnings at entities accounted for using the equity method and dividend income (mainly Telefónica).

- The repurchase of 51% of Servihabitat had a negative impact of €204 million, of which €152 million are reported under Other charges to provisions and €52 million under Gains/(losses) on disposal of assets and others. The loan loss provisions risk and other charges to provisions was down 57% on the same period of 2017, which included a number of one-off impacts in connection with early retirements and write-downs on the Sareb exposure.

- The contribution of BPI domestic business to the results amounted to €76 million. Including its investees, the total contribution by BPI was €252 million.

- CaixaBank Group’s fully-loaded Common Equity Tier 1 (CET1) ratio was 11.4%, within the target band of 11-12% envisioned in the Strategic Plan, and including the extraordinary impact of the repurchase of minority interests in BPI and a 51% stake at Servihabitat,. Total capital, fully loaded, came to 15.7%, above the stated 14.5% target.

The CaixaBank Group, chaired by Jordi Gual and managed by Gonzalo Gortázar (CEO), reported a net attributable profit of €1,298 million in the first half of 2018 (+54.6% year-on-year).

The main factors behind this growth were strength of core revenues, the reduction of provisions and higher income from BPI.

In addition, recurring administrative expenses, depreciation and amortisation increased by 4%, below the increase in core revenues (net interest income, fee and revenue from the insurance business), which amounted to €4,091 million (+4.5%). Gross income climbed by 8.7% to €4,654 million.

The contribution of BPI’s business in Portugal to the results amounted to €76 million (€3 million in the first half of 2017). Including its investees, the total contribution by the Portuguese bank was €252 million.

The CaixaBank Group’s profitability improved to 10.4% ROTE —consistent with the 9-11% target range set in the Strategic Plan for 2018— while recurring ROTE from the banking and insurance business segment was 12%, yielding a result of €1,121 million.

CaixaBank leads the mobile payments market in Spain, with close to 50% of total transactions

The Bank has continued to strengthen its leadership in digital banking, having amassed the largest base of digital customers in Spain: a market penetration of 32%, with 5.8 million digital customers (55% of total customers in Spain) and 5 million mobile banking customers.

CaixaBank was recently named Best Digital Bank in Western Europe by British magazine Euromoney due to its impressive digital transformation and technological innovation. This is the first time Euromoney has honoured CaixaBank with this accolade.

The Bank’s growth in mobile payments has been remarkable, climbing from 165,000 transactions in June 2017 to 2.2 million in June 2018, with an average transaction amount of 32.5 euros. Since January, the Bank’s customers have completed over 10 million transactions.

CaixaBank leads the mobile payments market in Spain, with close to 50% of total transactions. A total of 550,000 CaixaBank customers have now linked their cards to their mobile devices so they can pay using their phone. A total of 730,000 cards are now linked to mobile phones. These figures reveal significant customer growth of 53% since year-end 2017 (+190,000 customers with cards linked to mobile devices).

Meanwhile, imaginBank now has more than one million customers, just two years after its launch. CaixaBank’s mobile-only bank now has upwards of 120,000 customers using the service every day. imaginBank’s average customer is 23 years old and connects to the service 13 times per month.

Digitalisation enables a continuing focus on providing quality advice, with 13,170 qualified advisor-managers. For example, some 70% of premier banking and private banking customers now have an advisory services contract, while portfolios under management have grown 56% in the year.

Net interest income climbs to €2,432 million (+3.5%)

The Group’s net interest income in the first half of 2018 amounted to €2,432 million (+3.5% year on year), impacted by a higher return on lending activity, intensive management of retail financing and cost savings on institutional financing.

Fee and commission income climbed to €1,293 million, up 3.3% to the same period in the previous year. While banking services, securities and other fees were down 5.9%, fees on mutual funds continued to grow (+18.4%), as did fees on pension plans (+9.4%) and fees on sales of insurance products (+26.7%) following a steady increase in commercial activity and assets under management.

Extraordinary impacts on the results of investees

Income from equity investments totalled €415 million to the Group’s profit. This includes dividend income, mainly at Telefonica (€104 million), and earnings at entities accounted for using the equity method. It includes €118 million from BFA in net attributable profit. An attributable loss of €97 million was recognised in the same period in the previous year related to the sale by BPI of 2% of its stake in BFA.

Trading income climbed to €293 million, as a result of the materialisation of unrealised capital gains on financial assets available for sale, and the adjustments made to the selling price of BPI’s stake in Viacer, among other impacts.

Growth in lending and customer funds

Loans and advances to customers, gross, totalled €225,744 million at the Group (+0.8% in the year) and the performing portfolio was up 1.6% in the year to date (€+3,366 million). Excluding the seasonal impact of the prepayments made to pension holders in June (€+1,601 million), the performing portfolio has grown 0.8% in the year.

Performing loans to individuals has grown 1.2% in the year (+6.3% in the quarter), largely on the back of consumer lending in Spain (+5% in the quarter and +10.7% in the year).

Loans for home purchases continue to be affected by the ongoing household deleveraging process, although the outstanding balance on these loans is now falling at a slower pace. New mortgage loans happen to be up 7.9% on the first half of 2017.

Customer funds grew to €366,163 million at the end of June 2018, up 4.8% (€16,705 million), with 6.1% growth in on-balance sheet funds and 1.8% growth in assets under management, which amounted to €98,316 million (+1.2% in the quarter).

Demand deposits were up 8.6% in the second quarter to reach €175,960 million, following the seasonal impact of double salary payments and the early redemption of subordinated retail liabilities at the end of the quarter.

Meanwhile, assets under management climbed to €98,316 million (+1.2% in the quarter). Continuing the trend seen in recent quarters, the Group reported a sizeable increase in assets under management in mutual funds, managed accounts and SICAVs to reach €68,272 million (+1% in the quarter), mainly due to new subscriptions. Pension plans came to €30,044 million (-1.5% in the quarter).

The Group’s NPL ratio falls to 5.3%

The CaixaBank Group’s NPL ratio has now fallen to 5.3% (6% at December 2017 and 6.5% at June 2017).

Non-performing loans dropped to €12,714 million (down €981 million and €1,591 million in the quarter and from December, respectively), following the Group’s active management of problem assets, including the sale of portfolios.

The coverage ratio increased to 56% (+6 percentage points in the year, due, among other factors, to the adoption of IFRS 9, which has required the Group to post €791 million in provisions for credit losses).

Loan loss provisions risk and other charges to provisions were down 57% year on year to €531 million.

This heading comprises loan loss provisions, which fell to €248 million in the period (-47.5% year on year), as well as other charges to provisions, which were down 62.9% to €283 million. Since the deal to repurchase Servihabitat had yet to be completed at 30 June, the second quarter of 2018 included a provision of €152 million to cover the difference between the cost of buying back the 51% stake from TPG and the estimated fair value of that stake.

In 2017, this heading included €455 million in connection with early retirements (€152 million and €303 million in the first and second quarter of the year, respectively) and €154 million in write-downs on the Sareb exposure in the first quarter.

Gains/(losses) on disposal of assets and others mainly shows the results of completed one-off transactions and proceeds from asset sales and write-downs, primarily related to the real estate portfolio.

The change here was a result of positive proceeds of €151 million on the sale of real estate assets (+91.1%); other profit/(loss) from the real estate business (€-202 million), which includes allowances associated with asset valuations; and €52 million in impairment on 49% of the stake held in Servihabitat so as to bring its book value in line with its new fair value.

In the first half of 2017, this heading included the positive result related to the business combination with BPI (€256 million).

Deconsolidation of the real estate business

CaixaBank reached an agreement in the second quarter of 2018 to buy back 51% of the share capital of Servihabitat and thus regain control of its real estate servicer. The deal generated a negative result of €204 million in June 2018.

Meanwhile, CaixaBank has agreed to sell its real estate business (including mainly the portfolio of available-for-sale real estate assets at 31 October 2017, along with 100% of the share capital of Servihabitat) to a newco, 80% of which will be owned by Lone Star and the remaining 20% by CaixaBank. Completion of the deal will mark the deconsolidation of the real estate business and is estimated to have a neutral impact on the income statement.

The net book value of the portfolio of real estate assets available for sale at 30 June 2018, excluding those real estate assets to be sold under the previously described deal, is estimated at €522 million.

Sales of real estate assets total €1,143 million (+70.9%)

The portfolio of net foreclosed real estate assets available for sale stood at €5,553 million (€-705 million and €-257 million in the last 12 months and in the quarter, respectively). Real estate assets held for rent amounted to €2,806 million, down €224 million in the quarter, which included the sale of a portfolio of these assets.

Total sales of real estate assets came to €1,143 million in 2018 (+70.9% year on year), including the sale of rental assets valued at €226 million (+37.1 excluding this impact). The margin of sales to book value is 17% in the year to date.

Robust liquidity and solvency

Total liquid assets came to €79,892 million, up €7,117 million in the first half of the year. The Group’s average Liquidity Coverage Ratio (last 12 months) is now 199%, well clear of the minimum requirement of 100% from 1 January 2018 onward.

CaixaBank Group reported a fully-loaded Common Equity Tier 1 (CET1) ratio of 11.4 % at 30 June, within the target band envisioned in the 2015-2018 Strategic Plan (11-12%). Excluding the impact of -15 basis points due to the first-time adoption of IFRS 9 and the extraordinary impact of -23 basis points due to the repurchase of minority interests in BPI and the 51% stake in Servihabitat, the ratio gained 38 basis points in the first six months of the year from capital generation but shed 26 basis points due to prevailing market conditions and other factors.

Fully-loaded total capital was 15.7%, above the 14.5% target envisaged in the Strategic Plan