Caixabank (Go to Home)

Caixabank (Go to Home)

Print page

Print page

27 April 2018

|

min read

CORPORATE

National

VALENCIA

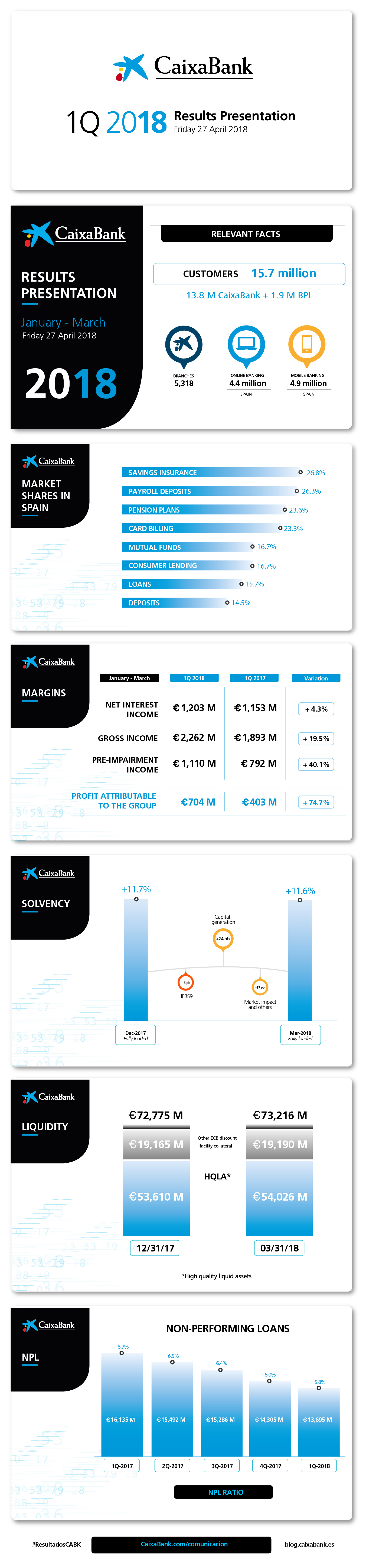

CaixaBank makes a profit of €704 million and improves its profitability to 9.8%

Gonzalo Gortázar, CEO of CaixaBank

Gonzalo Gortázar, CEO of CaixaBank

- The Group's results are based on increased income, with gross income up 19.5% to €2,262 million, driven by the strong performance of the core banking business (€2,008 million, up 6.5%).

- Non-performing loans fall by €610 million in the quarter (down €2,440 million over the last twelve months) with the NPL ratio falling to 5.8% (6.0% in December 2017). The coverage ratio increases to 55%.

- Customer funds amount to €351,420 million (+0.6% in 2018), and loans and advances to customers stand at €223,249 million (-0.3% in the quarter). The performing loan portfo-lio remains stable.

- The bank enhances its leadership in digital banking: market share stands at 33%; 56% of customers are digital; and imaginBank welcomes its one-millionth customer, just two years after its launch.

- Net interest income was up 4.3% to €1,203 million; fee and commission income totalled €625 million (+6.4%); and income and expense arising from insurance and reinsurance contracts climbed 24.9% to €138 million.

- Impairment losses on financial assets fell to €139 million, 44.3% lower than the same period in 2017 (stable compared to the previous quarter). Other charges to provisions fell by 86.3% (in 2017 these included extraordinary negative impacts relating to early retirement and write-downs of SAREB exposure).

- Total liquid assets stood at €73,216 million at 31 March 2018, an increase of €441 million in the quarter. The Group's average Liquidity Coverage Ratio (last 12 months) was 194%, well above the minimum of 100% required from 1 January 2018.

- The CaixaBank Group's fully loaded Common Equity Tier 1 (CET1) ratio was 11.6%, consistent with the range set in the Strategic Plan of 11%-12%, while total capital in fully loaded terms stood at 16.1%, exceeding the Strategic Plan target of 14.5%.

- Income from equity investments totalled €271 million. This includes earnings at entities accounted for using the equity method and dividend income.

- The contribution of BPI’s business to the results amounted to €40 million (€22 million in February and March 2017). Including its investees, the total contribution by BPI was €169 million.

The CaixaBank Group, chaired by Jordi Gual and managed by CEO Gonzalo Gortázar, reported net attributable profit of €704 million in the first quarter of 2018, up 74.7% year-on-year.

The main factors behind this growth were the strength of core revenues, the reduction of provisions and higher income from stakes.

In addition, recurring expenses increased by 5.4% (1.8% without including the BPI cost base), lagging the increase in core revenues (net interest income, fees and revenue from the insurance business), which amounted to €2,008 million (up 6.5%, or +3.7% excluding BPI). Gross income climbed by 19.5%, to €2,262 million.

The contribution of BPI’s business to the results amounted to €40 million (€22 million in February and March 2017). Including its investees, the total contribution by the Portuguese bank was €169 million.

The CaixaBank Group's profitability improved to 9.8% – consistent with the 9%-11% target range set in the Strategic Plan for 2018- while the recurring ROTE for banking and insurance business was 12%, with profit of €520 million.

CaixaBank bolstered its leadership of online banking and digitalisation

CaixaBank has cemented its leading position in the Spanish retail market. It is now the main bank for 26.7% of customers and ranks first in salary deposits (market share of 26.3%), investment funds (16.7%), pension plans (23.6%) and savings insurance (26.8%).

The bank is continuing to reinforce its leadership in online banking: market share of 33%; 56% of its customers are digital; and it has 4.9 million mobile-banking customers.

And, imaginBank now has more than one million customers, just two years after its launch. CaixaBank's mobile-only bank has 120,000 active customers per day. imaginBank's average customer is 26 years old and accesses the service 13 times per month.

imaginCafé opened in the centre of Barcelona in the middle of December last year. It is already attracting significant visitor numbers, averaging 800 people per day, and the trend is upwards.

Digitalisation enables a continuing focus on providing quality advice, with 10,900 managers having financial advice qualifications. For example, the mutual funds in the hands of customers who receive advice account for 83% of the total, with a 34% increase in managed accounts.

Net interest income climbs to €1,203 million (+4.3%)

The Group's net interest income in the first quarter of 2018 amounted to €1,203 million (+4.3% compared to the first quarter of 2017), impacted by the incorporation of BPI in February 2017, which contributed 2.1% of this growth.

Fee and commission income stood at €625 million, +6.4% compared to the same period in the previous year, following the integration of BPI, which contributed 5.4% of the growth. Compared to the first quarter of 2017, performance was impacted by lower fees from investment banking and higher fees from selling insurance and pension plan management.

Extraordinary impacts on the results of investees

Income from equity investments totalled €271 million. This includes earnings at entities accounted for using the equity method and dividend income. It includes €100 million from BFA (€76 million net attributable), following extraordinary impacts arising, amongst other things, from the devaluation of the Angolan currency. An attributable loss of €97 million was recognised in the same period in the previous year, due to the sale by BPI of 2% of its interest in BFA.

The net gain/(loss) on financial assets and liabilities and others increased to €136 million, as a result of latent gains on available-for-sale financial assets materialising and the revaluation of the sale price of BPI's interest in Viacer, which contributed €54 million to net attributable profit.

Revenue from insurance contracts grew by 24.9% compared to the same period in the previous year, to €138 million.

Recurring expenses amounted to €1,149 million, up 5.4% (+1.8% excluding incorporation of the cost base of BPI, compared to the same period in the previous year).

The gains/(losses) on disposal of assets and others essentially comprise the results of completed one-off transactions and proceeds from asset sales and write-downs mainly relating to the real estate portfolio.

Stable lending and customer funds

Customer funds in the Group increased by 0.6% to €351,420 million at the end of March 2018. On-balance sheet funds increased by 1.0%, with a 2.0% increase in demand deposits, to €162,020 million, and a sustained reduction in term deposits (-7.2%), to €33,230 million.

Assets under management increased to €97,171 million (+0.6% in the quarter), despite the negative performance of the market. Continuing the trend of recent quarters, there was an increase in assets managed in mutual funds, portfolios and SICAVs to €67,582 million (+1% in 2018), mainly due to new subscriptions.

CaixaBank is maintaining its leadership of this business segment, with a market share of 16.7% for mutual funds and 23.6% for pension plans.

Loans and advances to customers stood at €223,249 million at the end of the first quarter of 2018, 0.3% lower than in December 2017. The performing loans portfolio was stable in the quarter.

Loans for home purchases continued to be affected by the ongoing household deleveraging process, with new loans trailing loan repayments. Other loans to individuals gained 0.4% in the quarter, largely in response to growth in consumer loans (+5.3% in Spain in the year).

The Group's NPL ratio falls to 5.8%

The CaixaBank Group's non-performing loans ratio fell to 5.8% (6.0% in December 2017 and 6.7% in March 2017). Non-performing loans fell to €13,695 million (down €610 million and €2,440 million in the quarter and the last twelve months, respectively).

The coverage ratio increased to 55%. This was up 5 percentage points in the quarter, due, amongst other factors, to the implementation of IFRS 9 and the recognition of provisions for credit risk amounting to €758 million.

Impairment losses on financial assets fell to €139 million, 44.3% lower than the same period in 2017 (stable compared to the previous quarter).

Other charges to provisions primarily reflects the coverage needs for contingencies and other asset impairment allowances. The first quarter of 2017 included recognition of €152 million in connection with early retirements and €154 million in write-downs on SAREB exposure.

Sales of real estate assets total €306 million (+3.4%)

The net portfolio of available-for-sale foreclosed real estate assets stood at €5,810 million at the end of the quarter (down €475 million and €68 million in the last twelve months and quarter, respectively), with a coverage ratio of 58%.

Total real estate sales in 2018 reached €306 million (+3.4% compared to the same period in 2017). These sales have had a 16% impact on net book value in 2018.

Robust liquidity and solvency

Total liquid assets stood at €73,216 million at 31 March 2018, an increase of €441 million in the quarter. The Group's average Liquidity Coverage Ratio (last 12 months) was 194%, well above the minimum of 100% required from 1 January 2018.

The CaixaBank Group had a fully-loaded Common Equity Tier 1 (CET1) ratio of 11.6% at 31 March, within the target band envisioned in the 2015-2018 Strategic Plan (11%-12%), and almost 3 percentage points clear of the supervisory requirement of 8.75%.

Excluding the impact of the first application of IFRS 9 (-15 basis points), this ratio increased by 24 basis points in the quarter due to capital generation, and fell by 17 basis points due to changes in the market and other factors. Fully-loaded risk weighted assets (RWA) amounted to €148,328 million at the end of March 2018.

Meanwhile, fully-loaded total capital was 16.1%, exceeding the 14.5% target set in the Strategic Plan.

{kind=link}

{kind=link}